Brazil Import Tax Reform Explained

General Context

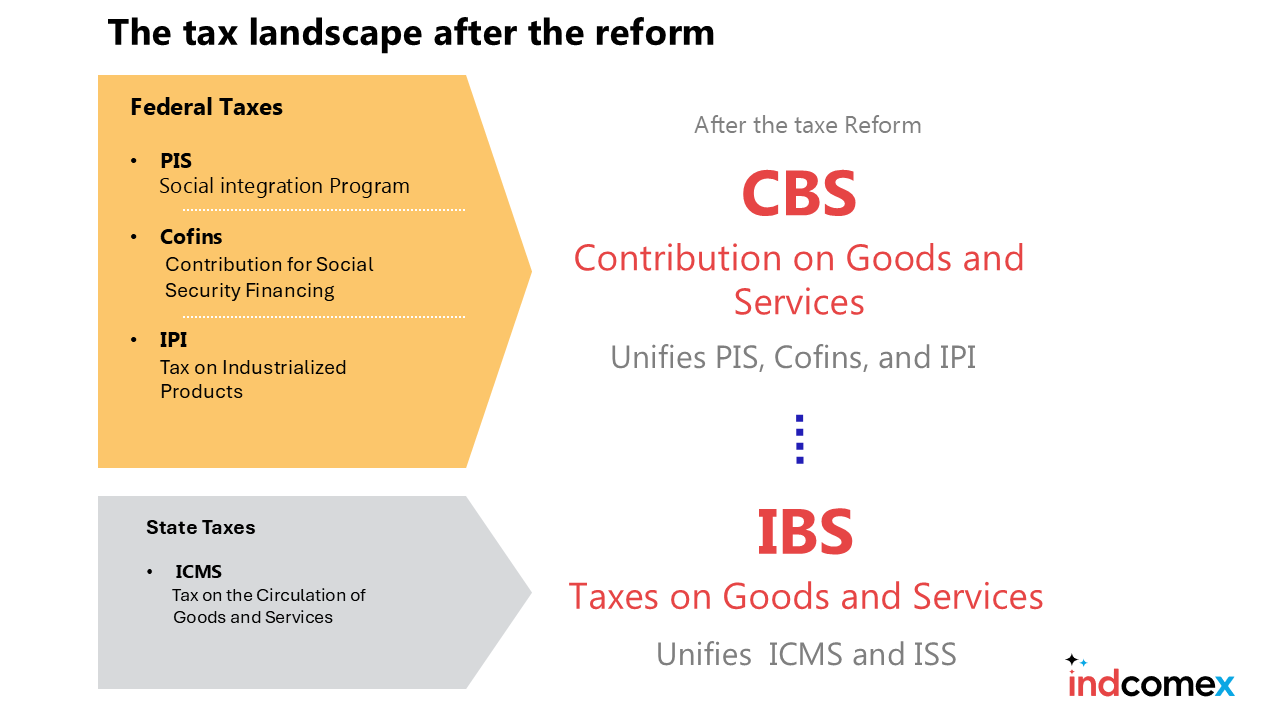

Brazil is replacing a complex group of consumption taxes with a simpler and more transparent model known as the Dual VAT.

Today the system includes PIS Cofins IPI ICMS and ISS.

These will be replaced by two taxes

IBS Tax on Goods and Services managed by states and municipalities

CBS Contribution on Goods and Services managed by the federal government

The intention is to reduce confusion, standardize rules and make taxation easier to understand for companies that buy, sell or import.

The country is moving toward a national style VAT with two coordinated components.

Main Objectives of the Reform

Simplify the system by eliminating five taxes and creating two

Make taxes more neutral and avoid interference with economic decisions

Increase transparency with external price calculation

Provide legal predictability and national standardization

What Are IBS CBS and the Selective Tax

IBS will be the unified state and municipal consumption tax replacing ICMS and ISS

CBS will replace PIS and Cofins with full credit and full non cumulative rules

A Selective Tax will also apply to products that harm health or the environment

Timeline from 2026 to 2033

2026 testing year

CBS will be 0.9% and IBS 0.1% only to run the systems without increasing tax burden

2027 and 2028 adjustment years

End of PIS and Cofins

CBS starts with full rate

IPI becomes almost zero outside the Manaus Free Zone and the Selective Tax begins

2029 to 2032 transition

ICMS and ISS fall gradually

The participation of IBS increases as the model matures

2033 full model

ICMS and ISS are extinguished

IBS and CBS become the only consumption taxes in Brazil

Estimated Rates of the New VAT

Government projections indicate

CBS close to 8.8%

IBS close to 17.7%

Total VAT around 26.5% to 28%

Some essential sectors will have reduced rates

For Chinese readers it is reasonable to consider a base VAT of about 27% with lower rates for essential goods

Main Advantages of the Reform

Brazilian and foreign companies including Chinese suppliers will benefit from several improvements

Fewer taxes to understand

Broader and recoverable financial credits

Greater predictability of costs

End of the tax competition between states

Clearer rules and unified calculation across the country

How Importation Works Under the New Model

II import duty remains the same

IPI almost disappears for products without local production incentives

IBS and CBS will apply to all imported goods

The new tax base includes

customs value

freight

insurance

II

fees

Selective Tax if applicable

The calculation is external which avoids tax on top of tax

Clearance at customs may appear more expensive at the moment of importation but credits throughout the supply chain tend to compensate part of the impact

If you want to know the exact effect on your product our import calculator is already prepared to simulate both the current and the new model side by side. Click here to use it

End of the Fiscal War and New Logistics Logic

Without ICMS at origin states no longer compete by offering incentives

Port and distribution center choices will reflect real logistics efficiency rather than state discounts

The country moves closer to international practice and offers more predictability

How to Prepare Now

Map your product NCM correctly

Simulate new scenarios with IBS and CBS

Adjust fiscal and commercial systems

Review logistics operations

Follow the complementary laws under discussion

If you need to check the NCM of a product IndComex offers an advanced search with chapters breakdown and tax rates. Click here to access the NCM list

Conclusion

The Tax Reform changes prices logistics importation and the general functioning of consumption in Brazil. It is a long transition but necessary to reduce complexity and strengthen competitiveness.

If you want to understand the exact impact on your product your import process or your business operation we offer specialized consulting and personalized analysis.

Related Blog